Many individuals are surprised to learn that their vision and dental plans are often purchased separately from their standard health insurance. This separation has deep historical roots and continues to influence how these benefits are structured and regulated today. Understanding the reasons behind this division can help you make more informed decisions about your healthcare coverage and budget.

Once considered optional enhancements, vision and dental insurances are now recognized as distinct types of coverage, each with its own networks and regulatory frameworks. This separation offers both advantages and challenges, affecting everything from premium costs to the providers you see. Grasping these differences is essential for effective healthcare planning, especially as the landscape evolves with new policies and market trends.

In this article, we will explore why vision and dental insurance are separate from general health coverage, how they developed historically, and what that means for consumers today. We’ll also look at how these plans are offered, their benefits, and the potential for integrating coverage in the future.

Why Medical, Vision, and Dental Are Treated as Separate Fields

Dental and vision care have historically operated independently of general medical services. In earlier centuries, dental procedures were performed by barbers or general practitioners who also handled other medical tasks such as bloodletting or wound care. Dentistry only began to establish itself as a specialized field in the mid-19th century with the creation of dedicated dental schools. This formal training and specialization further distinguished oral health from general medicine.

Similarly, vision care was historically provided by craftsmen who made and sold glasses, rather than medical professionals. This craft-based approach created an early divide between vision correction and healthcare. Over time, as organized health systems developed, the separation was reinforced by insurance practices. Many employers negotiated with unions to include eye and oral health benefits as supplemental offerings beyond their existing medical plans, emphasizing periodic rather than emergency care. According to Samuel Greenes, CEO of BLUE Insurance, this division persists because it allows for tailored coverage and cost management.

It’s important to note that health insurance may only cover dental work if it’s deemed serious enough to require hospitalization or emergency treatment due to injury or accident. Routine dental procedures like cleanings, fillings, or crowns are typically excluded from standard health plans, which is part of why separate dental plans have emerged.

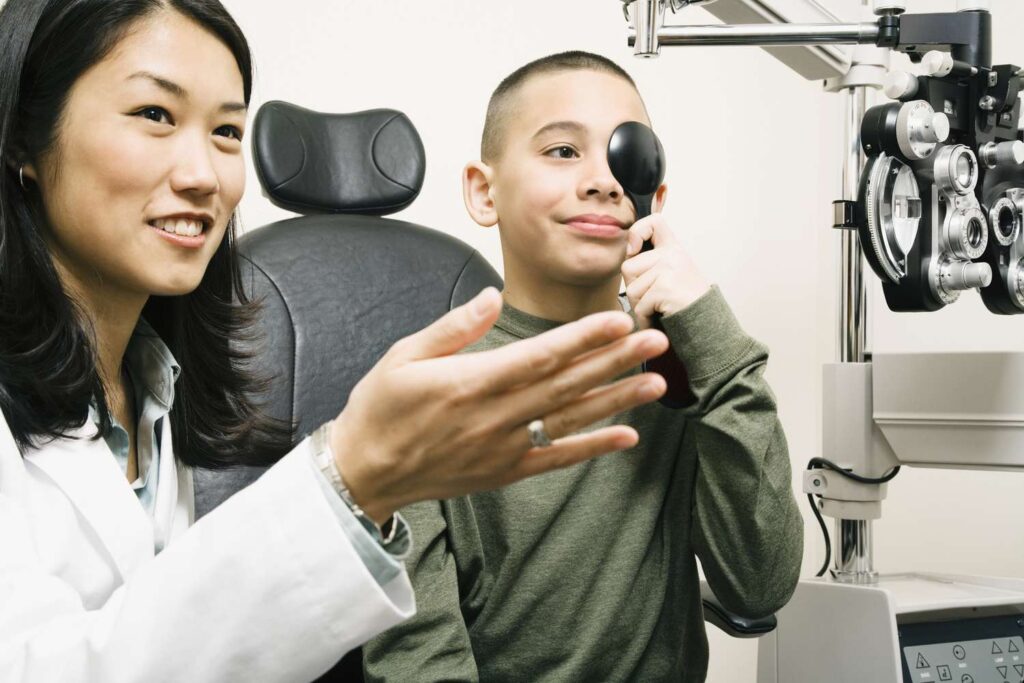

How Vision and Dental Insurance Differ from Medical Coverage

When it comes to eye health, health insurance generally covers issues related to infections, complications from diabetes, or other medical conditions affecting the eyes. These plans may also cover prescriptions related to eye health. However, routine services such as eye exams, glasses, or contact lenses are usually covered only by vision insurance plans. Not all vision policies include annual contact lens evaluations, so it’s essential to review your coverage details carefully.

The structure of these plans also differs significantly. Standard health insurance plans often contract with a wide network of physicians, specialists, and hospitals. However, they typically do not include extensive networks of oral and vision care providers. Conversely, dental and vision insurers maintain their own networks of specialists, including dentists, orthodontists, ophthalmologists, and optometrists, to deliver targeted services at reduced costs.

Practical Tip

Make sure your eye care provider participates in both your health and vision insurance networks. For example, if your eye specialist detects a medical condition like glaucoma during a routine exam, they would bill your health insurance for that visit, while routine eye exams are billed through your vision plan. This dual-network approach helps you maximize coverage and manage costs effectively.

The Rationale for Keeping Vision and Dental Plans as Supplemental Benefits

Insurance companies classify vision, dental, and pharmacy plans as supplemental benefits because they typically involve lower per-service costs compared to comprehensive hospital or physician coverage. This classification allows insurers to establish separate networks and administrative structures, making these plans more manageable and cost-effective.

Interesting:

- Uncovering why eye care is often excluded from insurance coverage

- Comprehensive guide to healthcare and health insurance for expats in austria

- Clarifying the distinction between healthcare stipends and health insurance

- The connection between employment and health coverage in the u s

- Understanding the differences between private and public health insurance

While these plans are often sold separately, there is increasing interest in bundling them with traditional health insurance to simplify enrollment and billing. However, current regulations under the Affordable Care Act (ACA) treat adult dental and vision benefits as non-essential, which means they are optional and usually not included in standard health plans. This classification encourages insurers to offer them as standalone policies, giving consumers more flexibility but also requiring careful planning to ensure comprehensive coverage.

Important Notice

Discount plans that offer reduced rates on dental and vision services are different from full insurance policies that cover diagnostic, preventive, and restorative procedures. You cannot use both a discount plan and insurance for the same procedure, which is an important consideration when choosing coverage options.

Accessing Vision and Dental Benefits through the Marketplace and Federal Programs

You can purchase vision and dental coverage through the health insurance marketplace, but not all plans include these benefits. These services are often excluded from the list of the 10 essential health benefits mandated by the ACA. Consequently, some plans may omit vision or dental coverage altogether, making it crucial to review your options carefully.

The Federal Employee Dental and Vision Insurance Program (FEDVIP) offers coverage to federal and postal employees, retirees, and their families. Premiums for FEDVIP are paid out of pocket, often with group discounts that make the plans affordable. For instance, average monthly costs are approximately $35 for dental PPO plans and $14 for vision plans. These plans have no pre-existing condition limitations and allow employees to pay premiums through pre-tax payroll deductions.

Which Dental Plans Are Most Popular?

Preferred Provider Organization (PPO) plans dominate the dental insurance market. They typically offer larger provider networks compared to Health Maintenance Organization (HMO) plans, increasing the likelihood that your preferred dentist participates. Although out-of-network services are available with higher out-of-pocket costs, PPO plans offer greater flexibility.

Top Vision Insurance Providers

VSP is the largest vision insurer nationwide, serving over 80 million members with a network of more than 36,000 eye care professionals. Bundling dental and vision coverage is possible through many providers, including major insurers like MetLife and UnitedHealthcare, which often offer combined plans to simplify coverage and potentially reduce costs.

Final Thoughts: The Future of Vision and Dental Coverage

The separation of dental and vision benefits from general health coverage has historical roots that continue to influence current policies. This division allows insurers to keep premiums lower and provides consumers with tailored options, but it can also lead to gaps in comprehensive healthcare coverage.

Recent trends suggest a growing interest in integrating these benefits into broader health plans, but as of now, adult dental and vision services remain classified as supplementary. Staying informed about your options—whether through employer-sponsored plans, marketplace policies, or federal programs—can help ensure you receive the coverage needed for healthy eyes and teeth.

For a deeper understanding of how healthcare systems operate globally, including China’s expanding healthcare expenditures, visit understanding chinas healthcare system a comprehensive overview. Additionally, exploring the nuances of professional development credits can help you stay compliant and informed, which is vital when navigating specialized insurance plans. Learn more about the differences between CEU and CE credits in professional development.